.svg)

The Financial Services Pendulum: From Unbundling to Re-Bundling

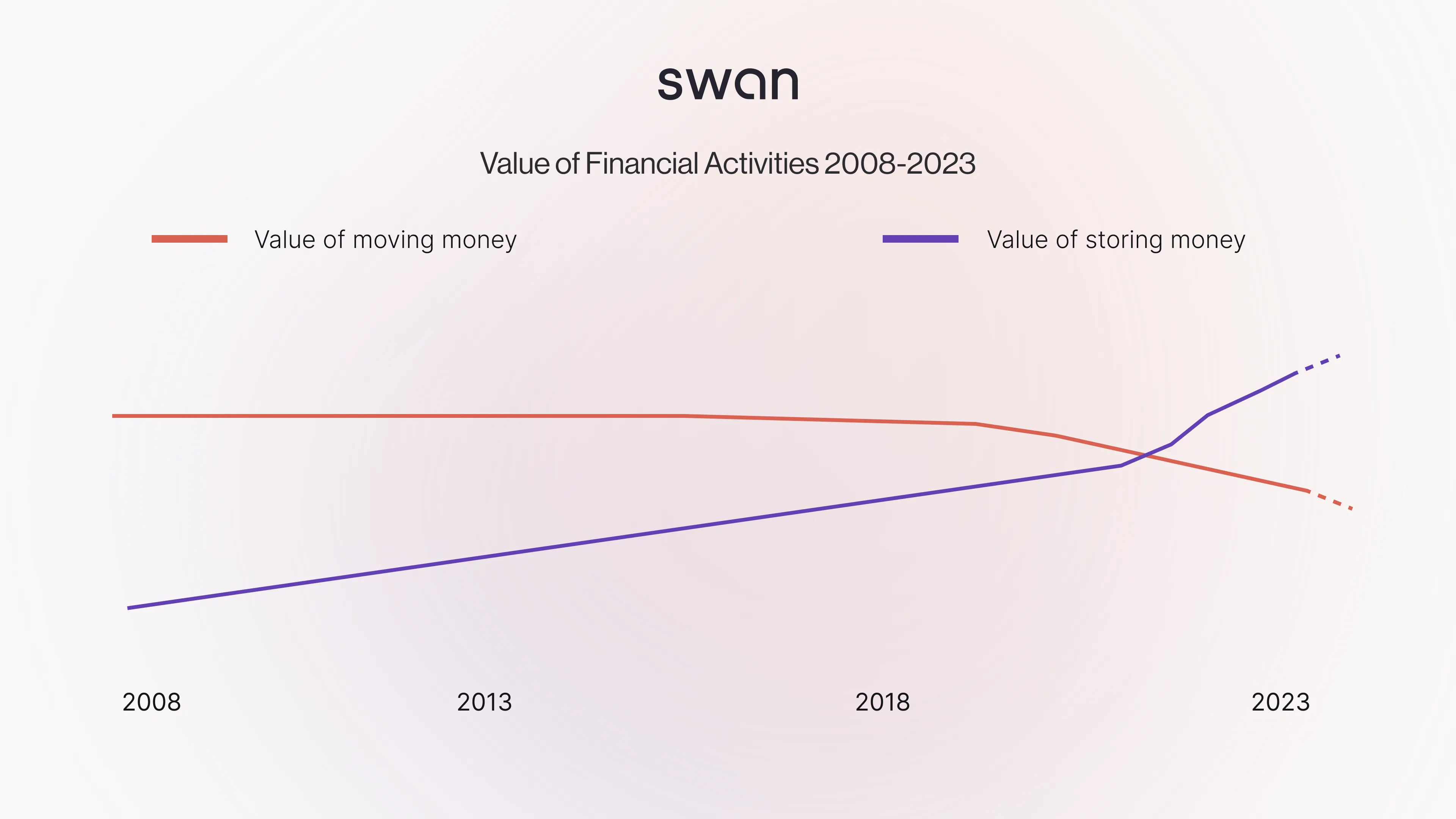

In a world of meaningful interest rates, what happens to companies focusing mostly on moving, rather than storing, money?

500,000

homeowners communities managed

80%

of property managers in Spain using it

40%

reduction of banking cost for communities

In the world of finance, trends come and go, and sometimes they come full circle. Fifteen years ago, the financial services industry saw a seismic shift as tech firms began to unbundle traditional banking services. Firms became specialized, seeking to excel in a single aspect of moving money. Stripe conquered card payment collection, Wise dominated the foreign exchange market, and a host of other companies emerged, each carving out their own niche.

This unbundling trend was representative of the low-interest rate environment of the 2010s. In the most basic sense, there was no money in storing cash. By intention, post 2008, the world economy was supercharged by a regime of near-zero interest rates. Money wanted to be moved, rather than stored.

At its core, a bank is focused on storage. An account for individuals or organizations is the fundamental unit of a bank. But banks do more than just look after money. They bundle services. Banks can transfer money for you, give you a mortgage, and do payment acquiring for your business, among other things.

These three activities were once handled solely by big ‘universal’ banks like HSBC, Citi, and Santander. But then, something changed. People started building companies to do just one aspect of ‘move money’ exceptionally well, by leveraging the internet.

Fintech entrepreneurs were convinced that they could move money better than incumbent banks and financial institutions, who were good at non-tech things like taking deposits and doing investment banking. When it came to more complicated activities, like enabling small businesses to trade online, banks’ offerings were far from excellent.

The first generation of money movers, represented in this article by Stripe, dedicated themselves to collecting money to only immediately give it away. This was new. They built superior payment processing because they could do it better than banks.

Focusing solely on money movement has recently become challenging. High interest rates have reduced transaction volumes and have made borrowing to finance growth more expensive while simultaneously making money storage more economically rewarding.

In a world with meaningful interest rates, financial services providers need to be focused on storage too. Apple in their unique way has already started (re)bundling. We see a future where most successful money movers start also storing money. They will largely replicate the bundle of services ‘universal’ banks offer but do it more usefully and efficiently. The modularity offered by BaaS providers will enable this new way of bringing financial services to market.

The post 2008 unbundling of financial services

Stripe was founded in 2010 by Irish brothers Patrick and John Collison with the ambitious goal of simplifying online payments. By enabling businesses to accept digital payments with minimal friction, Stripe sought to break down barriers for firms trading online.

Incumbent banks' payment solutions were insufficient for the needs of the burgeoning digital economy. Hindered by legacy systems, complex regulatory environments, and a lack of innovation, these traditional financial institutions found themselves struggling to adapt to the e-commerce blow-up.

Consequently, vendors were juggling high fees, convoluted user experiences, and limited global reach. It was amidst this chaos that Stripe started providing a comprehensive, user-friendly payment infrastructure tailored to the digital age.

The company's timing was impeccable, as it entered the market during an era of near-zero interest rates. This unique economic environment made orchestrating money movement more financially attractive than merely storing it.

In this economic climate, accumulation of capital for its own sake lost its luster, as returns were minimal.

Pre-2008, it would have been a non-starter to build a business around the idea of collecting money from a customer and then quickly releasing it to a merchant. But this was a new paradigm where the value of a dollar or euro sitting in an account was less than that of one on the go.

The math demonstrates it crystal clearly. When Stripe was first launched, it generally charged merchants a flat rate of 2.9% +30 cents per successful transaction. If you’re saying to yourself, that doesn’t sound very cheap, you’re right. But more to the point: extracting ~3% of the value of a money movement event, when you collect interest of only 0.25% on deposited cash, it is easy to see how the low interest rate environment could so strongly influence what type of businesses were viable.

It’s also worth mentioning that most of the planet enjoyed a wildly prosperous economic situation from 2010 through 2022. That folks had money to buy stuff was super helpful for the growth of these money movers. In fact, the money movers were so good at their jobs that they literally contributed to widespread economic growth (read: more sales) with their superior solutions. Or, to quote the motto of Stripe, they “increased the GDP of the internet”.

The success of Stripe can be attributed to a confluence of factors: the inefficiencies of traditional payment systems offered by incumbent banks, the favorable economic conditions brought about by near-zero interest rates, and the company's own innovative and user-friendly payment platform.

Money movers have been all the rage. They have benefitted from and contributed to torrid economic growth and a period of ‘easy’ money supported by low interest rates. But this Gestalt was not going to hold forever. Something had to give…

Just moving money... does it work?

In recent years, we've witnessed a boom in fintech companies specializing in the movement of money, seizing opportunities created by near-zero interest rates. But what happens when the pendulum swings the other way, and interest rates begin to rise?

Once prices began climbing and central banks across the world sought to reduce inflation by raising rates, people suddenly had less money to spend on stuff. Consumers and businesses alike tightened their purse strings. For companies whose bread and butter is moving money, this directly impacts the bottom line.

Borrowing costs also rise when interest rates go up. For fintechs that borrow funds to move money, this hurts. Margin compression puts a lot of pressure on companies. Prices might have to rise to compensate, which often leads to firms losing their competitive edge.

Finally, in a high-interest-rate world, the value proposition of money storage services becomes more attractive, as deposits can generate higher returns. It’s better in such a world to both store and move money.

In light of these challenges, it is essential for money movement-focused companies to remain agile and adaptable in the face of changing economic conditions. It just doesn’t make sense anymore to collect money to just release it immediately once again.

We believe that the next generation of successful financial firms will be those that successfully ‘re-bundle’ and figure out how to do some aspects of money movement and storage well. Embedded finance could likely be a great way to do this.

Re-bundling financial services is the future

Apple’s recent push into consumer banking is a great example of re-bundling. Apple first launched their credit card product Apple Card in August of 2019. They partnered with Goldman Sachs to act as the issuing bank and the card uses Mastercard’s payment network.

Apple Card is a product of the ‘move money’ era. It was designed to primarily live in the Apple Wallet and makes payments seamless for consumers both on- and offline.

The card holder spends with Apple Card, then pays their bill using a linked checking account at their bank of choice.

There is no storage of money involved whatsoever. In fact, it is perhaps more of an app than an actual credit card. Its purpose is primarily to drive adoption of Apple Pay as the preferred payment method for iPhone users, to increase overall stickiness of the Apple ecosystem, and generate a bit of revenue.

The new savings account from Apple upends this completely. Apple wants their users to also store their money in a dedicated savings account. The world’s most valuable company wants to get into the business of money storage now. They want iPhone users to forget about who they bank with entirely.

Are banks on the verge of extinction?

Combining money movement and money storage capabilities is not just for huge corporations. Companies that bring to market excellent solutions for both moving and storing money will begin to resemble the universal banks of the past.

But they will be different. Their products will be better, more attuned to the needs of end customers. BaaS providers offer modularity, so companies looking to embed banking features can pick and choose only those that they need.

We predict that this re-bundling of money movement and storage capabilities could kill the classic bank business model.

Before the financial crisis, only banks offered financial services (yes, we are generalizing a bit). Post 2008, startups began popping up, focusing on doing a small aspect of moving money excellently. Banks continued to exist, with the value proposition that they were a familiar one-stop shop for all consumers’ financial needs.

In the re-bundling that is to come, fintechs will leverage embedded finance to build markedly better experiences for customers that want to both move and store money. Their solutions will be faster, safer, and cheaper than those from incumbent banks.

Will legacy banks be dead men walking in this new world of meaningful interest rates, focused fintechs, and modular embedded finance? Let’s see what the future holds.

Summary

Customer stories

How Europe’s leading business platforms use Swan

.svg)

.svg)

%201.svg)

500+

Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

500+

Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

500+

Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

To use Apple Pay you need a supported card from a participating card issuer. To check if your card is compatible with Apple Pay, contact your card issuer. Apple Pay is not available in all markets. View Apple Pay countries and regions. Features are subject to change. Some features, applications, and services may not be available in all regions or all languages and may require specific hardware and software. For more information, see Feature Availability.