.svg)

Wielding embedded finance to perfect Expense Management

A look at how embedding card features will strengthen your expense management offering.

500,000

homeowners communities managed

80%

of property managers in Spain using it

40%

reduction of banking cost for communities

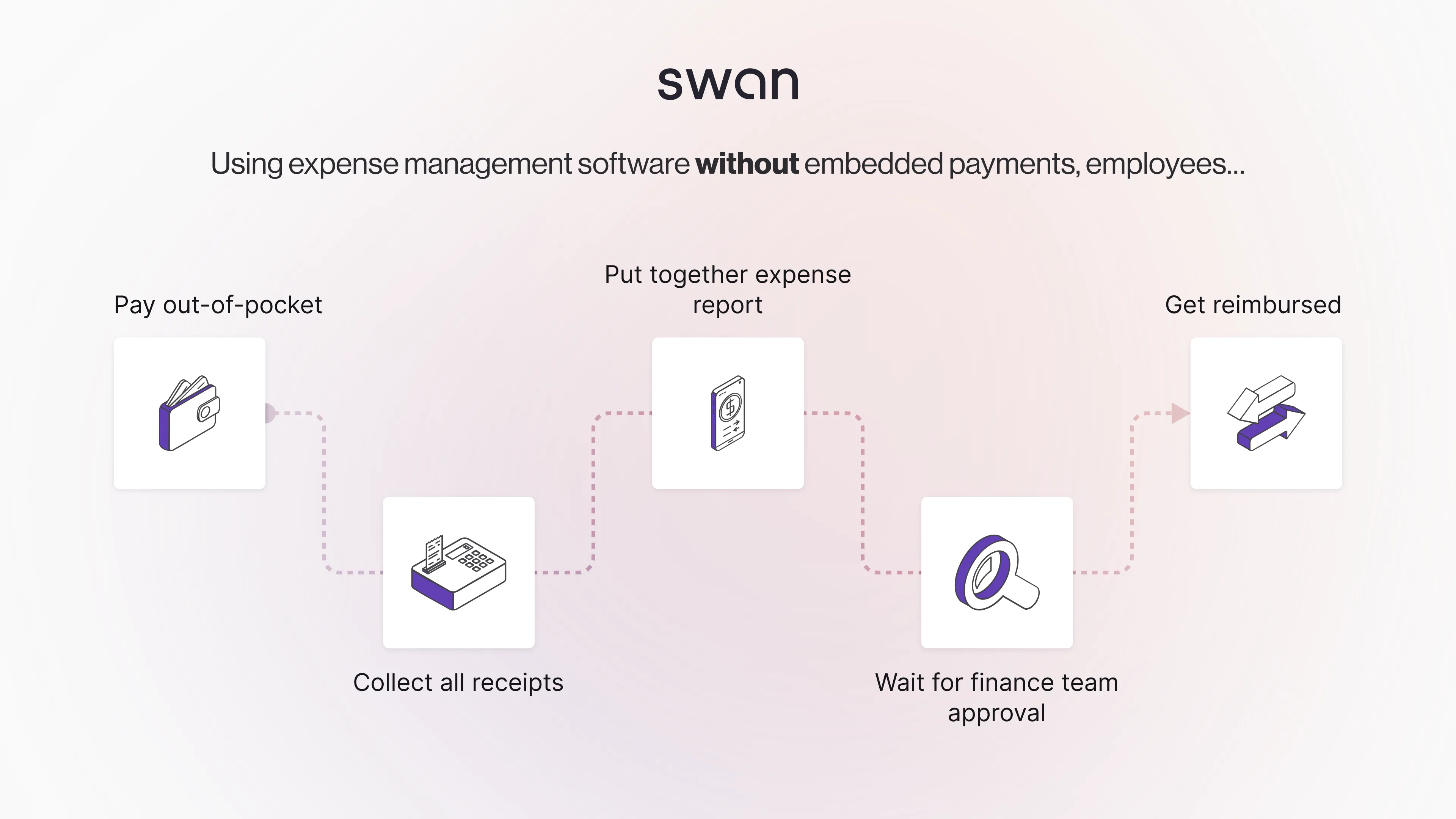

Many companies providing expense management solutions are looking to enhance their offering to solve a greater number of customer pain points. Employees needing to pay out-of-pocket, administrators spending an absurd amount of time managing expenses, and managers struggling to ensure financial control are just some addressable pain points. To build useful solutions, we think it’s crucial to grasp what is going on beneath the surface of expense management.

Let’s zero-in on what happens when an employee makes an expense payment. The moment a payment is made, the transaction kicks off a sequence of processes & workflows that finance teams must take care of: checking that it fits with the budget/expense policy, tracking & justification of payments, and processing VAT claims. The funds themselves move, but crucial data about the expenses must also reach the right people at the right time. Software enables this; embedding finance perfects it.

The workflows underpinning expense management

Historically, the management of expenses has been rather manual and rife with inefficiencies. The ability to process payment data to foster a deeper understanding of a company’s financial situation was more or less nonexistent. Recently, solutions have emerged to tackle this. Initially, the move was to partner with a card issuer– American Express is the leader in this segment– and then allocate cards to employees, who would be obliged to spend within a certain monthly limit and to justify every transaction. On the back-end, finance managers would have access to spending data, but would have to input and model the figures in Microsoft Excel or something similar. Such an approach has been adopted on the enterprise level pretty widely, but SMEs were left to fend for themselves without a useful technological solution.

Then, as the vertical SaaS revolution took hold, expense management software was developed to handle the processing and analysis of payments made by employees. Firms like Coupa, Rydoo, and Notilus built tools to simplify the submission of expense reports, apply rules, and set up validation workflows. Crucially, the carrying out of the payment itself was not facilitated through tech owned by these providers. Usually, the payments were made using the employee's personal card. Sometimes, especially within large enterprises, finance teams would craft a way to combine expense management software with corporate cards, though, again, this was by no means the norm amongst small companies. Nonetheless, payment data was not natively integrated with the wider software offering and processes were far from optimal.

Expense management SaaS firms, at least those founded in the last decade, did not have the opportunity to embed payments in their offerings initially. Limited by technical, financial, and legal conditions, these companies focused on building other products, such as OCR scanning and digital ledgers for accounting. However, after a few years, these firms began to witness the rise of the next generation of spend management solutions, who had cards and payments as core, primary features. Companies like Spendesk and Pleo built their offerings around two fundamental workflows: 1) lightning quick and accurate automatic processing of receipts and invoices and 2) the simple and fast issuing of cards, either virtual or physical, for employees to pay for all sorts of expenses.

Now, with embedded finance offerings popping up in the market, companies building expense management solutions can vastly expand their product suite. Payment capabilities can and should become core elements of firms’ offerings. By embedding banking features, it is possible to integrate previously discrete workflows into one, synergized offering.

Let’s dive deeper into some common workflows that are enhanced via embedded finance features.

How embedded finance can help with receipt processing

Business transactions can be largely split into two categories: Spend and Expenses. Spend refers to payments for things related to the overall business, such as supplier bills. Expenses are typically payments made by individuals or small teams for items that come up in the course of day-to-day operations (a taxi, coffee and croissants for a prospective customer).

Let’s focus on a hypothetical expense use case. We can imagine, for this exercise, the CRO of a company taking the CEO of a potential customer out to lunch.

Now, in the most traditional set-up, the CRO would simply pay for the meal using their own personal card or even via cheque or cash. The executive would then have to save the receipt, for there to be any chance whatsoever of receiving reimbursement. Then, at the end of the month or quarter, the CRO would submit his expenses with the accompanying receipts to finance, who would have to manually process each transaction one-by-one, with little to no tooling to help. With such long feedback loops and unsophisticated tooling, the opportunity for error or fraud is unnecessarily huge. Better integrated tech can solve this.

The processing flow is a bit better if an expense management solution has been deployed. Then, the executive can upload his receipt immediately for processing. Best-of-breed software would then seamlessly pull all the necessary data from the receipt: name of vendor, the cost of the good or service, when the transaction occurred, etc.

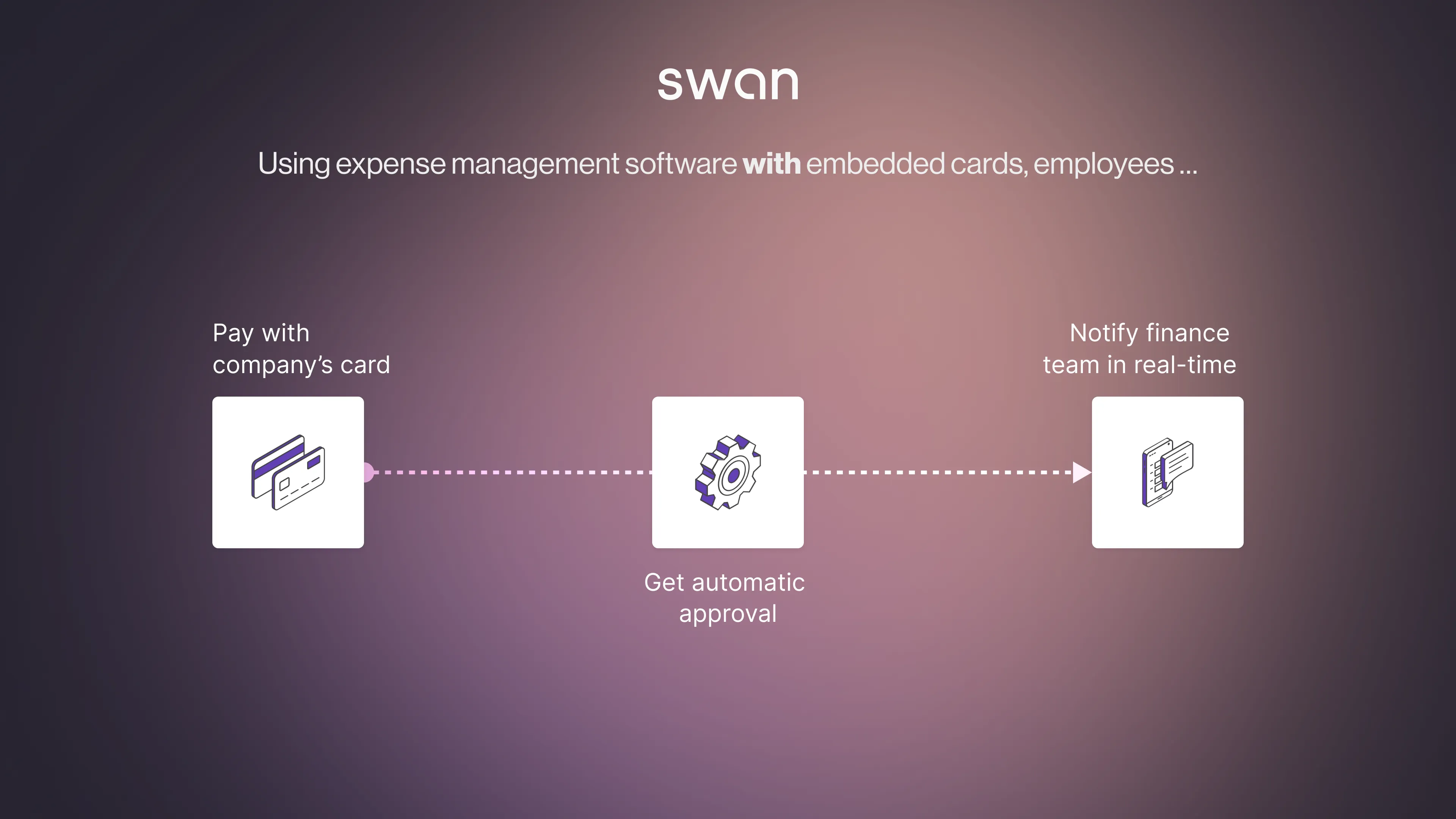

Simply put, the addition of embedded banking features to this workflow changes the game entirely. If the executive was instead in possession of a card linked directly to the company treasury, the processing of the invoice or receipt would proceed seamlessly. The finance team would automatically be aware of all the details of the transaction; all that information is already neatly organized in the finance team’s cockpit, delivered using embedded banking APIs.

How embedded finance can help with ensuring financial control

Embedded finance also touches the creation of expense policies and rules. Traditionally, employees would front purchases and submit expense reports to be paid back. In this paradigm, finance teams have essentially no ability to enforce expense policies until after the transactions occur. With cards from Swan, it is possible to ensure control from the very beginning.

Embedded cards allow for highly flexible rules and policies that extend to the transaction level. Finance teams can build payment control, so that a manager has complete visibility on their direct report’s spending. Further, it is possible to configure the cards so that only a certain category of expense, such as travel or transport, is approved. In this case, if the cardholder tried to buy a coffee, the card would be declined automatically at the point-of-sale.

Naturally, this control extends to budgeting as well. A manager can easily enforce a budget of, say, 500 EUR, for a more junior team member while their deputy could be approved to spend 3,000 EUR. By embedding cards in your expense management offering, the ability to set and enforce rules crucially lies before the transaction is made, thus eliminating a great deal of nasty and unnecessary administration after the fact.

How embedded finance can help generate revenue via shared interchange

Adding embedded banking enabled features makes your product offering more robust. But it can also be a meaningful source of additional revenue. As you may already know, the card networks (the Mastercards and Visas of the world) charge fees whenever a merchant accepts a transaction. This is called interchange.

As a partner of Mastercard, Swan receives a share of the revenue generated from transactions made with our cards. By embedding our card payments into your expense management solution, you too will receive a share of all interchange revenue generated by your end users.

We believe that by adding cards and having access to revenue from interchange, companies developing expense management tooling can triple their Average Revenue per User (ARPU). With the changing macroeconomic situation, in which there is a greater focus on profitability, adding a revenue driver with near unlimited scaling potential is a great idea indeed. Simply, the more your customers spend, the more you stand to earn!

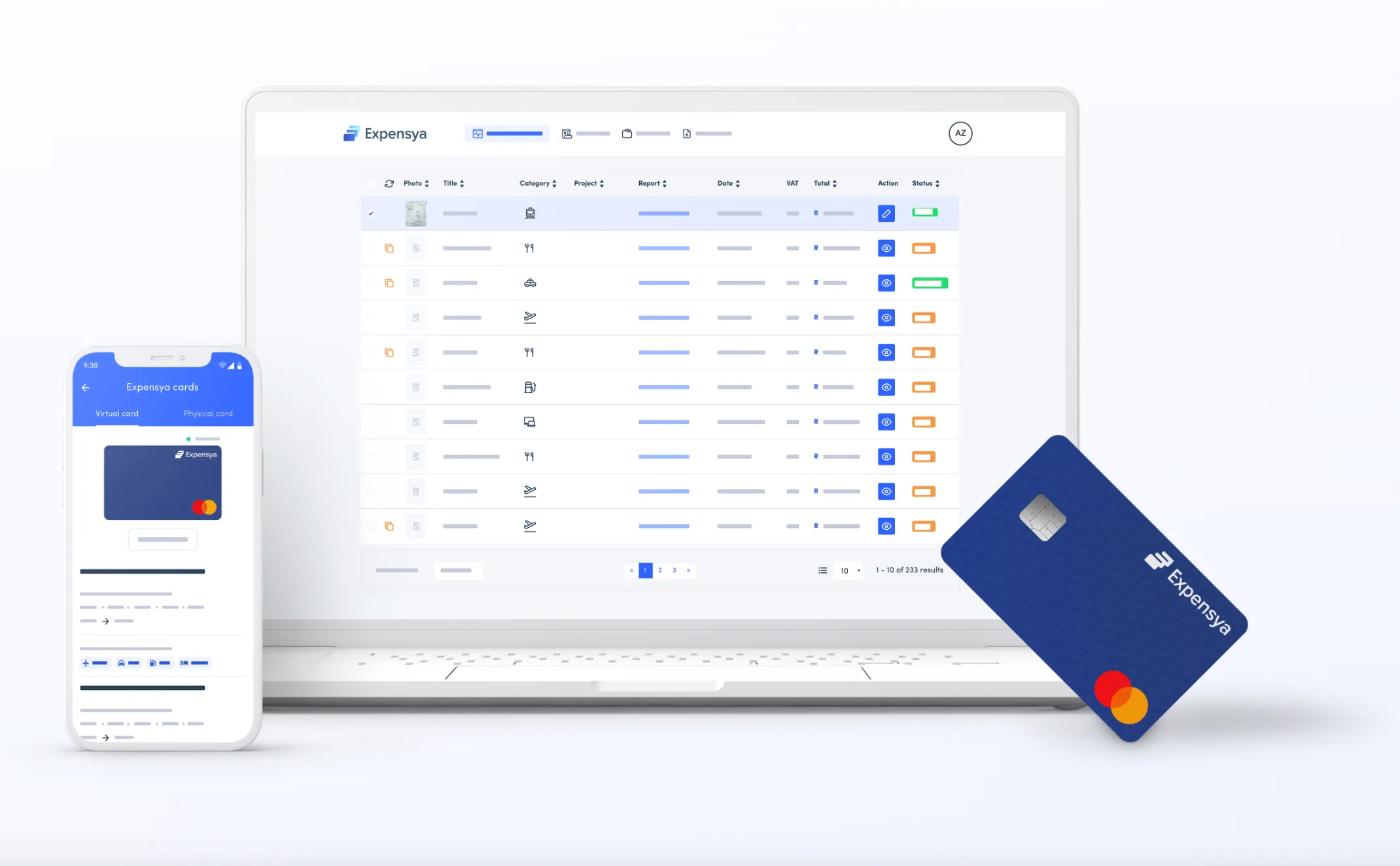

Adding cards has been game-changing for Expensya

Expensya is a leading expense management tool with a comprehensive set of products and features that allow over 6,000 customers to control and manage their employees’ spend. The firm’s offering empowers finance teams to eliminate manual processing of invoices, set spending rules, and enjoy visibility into what the company is spending cash on. Expensya integrates with other software providers, like SAP and Egencia, allowing users to streamline the entire accounting process.

Partnering with Swan, Expenya provides payment cards that employees of their customers can use to make transactions that finance teams can easily manage and understand. Employees feel trusted to manage their expenses while managers and finance teams can reduce manual work, take advantage of a far simpler workflow, and enjoy full visibility into firm-wide spend.

Expensya has seen remarkable success since introducing cards as part of their offering. In the second half of 2022, the company more than quadrupled the volume of transactions it handled. At the same time, physical cards in circulation grew by over 200%, even though only a low double-digit percentage of its customers have taken up cards. Moving into 2023, Expensya expects to make use of embedded finance to retain existing customers, attract new ones, and continue building up a sizable source of revenue via shared interchange. The sky’s really the limit for how embedded finance can change your business for the better!

Oh, the places you’ll go!

Embedding banking products like cards into your expense management tool is a game-changer. Receipt and invoice processing is considerably simplified. Instead of having to chase down every employee for their receipts, information about the transaction is recorded and saved automatically when the card is swiped. Setting rules and validations for employee spend is made much easier by embedding cards. Managers can directly control budgets, what types of products can be purchased, and so on, directly from the software cockpit.

On the business side, by issuing cards, expense management software providers can unlock a new revenue stream, in the form of interchange. As mentioned, we think you can roughly triple your ARPU by embedding cards into your platform. As you scale, and more payments are made with your cards, revenue generated from interchange will scale with you.

The potential of embedded finance is only beginning to be realized, so the future promises to be only more exciting! Here at Swan we are working on multiplying and improving what can be embedded into existing software solutions. You can already add physical, virtual, and single-use cards to your product and give your customers the considerable workflow advantages that come with that. Your product will be stickier, and your customers will be happier. A true win-win.

If you want to understand how much embedded finance can contribute to profitability, have a look at our calculator below.

Summary

Customer stories

How Europe’s leading business platforms use Swan

.svg)

.svg)

%201.svg)

500+

Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

500+

Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

500+

Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

To use Apple Pay you need a supported card from a participating card issuer. To check if your card is compatible with Apple Pay, contact your card issuer. Apple Pay is not available in all markets. View Apple Pay countries and regions. Features are subject to change. Some features, applications, and services may not be available in all regions or all languages and may require specific hardware and software. For more information, see Feature Availability.