.svg)

Open Banking & Embedded Finance: delivering financial services with the best UX

Discover how Open Banking and Embedded Finance are revolutionizing financial services with superior user experiences.

500,000

homeowners communities managed

80%

of property managers in Spain using it

40%

reduction of banking cost for communities

In the ever-evolving landscape of financial services, two concepts have emerged as transformative forces: Open Banking and Embedded Finance.

Open Banking is like opening a window into the world of banking, allowing customers to access and share their financial data with third-party providers. Embedded Finance, on the other hand, is like building an entire house with all the necessary banking functionalities, which can be customized and integrated into various applications or platforms.

Open Banking, explained

Open Banking, a term that has become increasingly familiar, is the practice of banks sharing financial information electronically, securely, and only under conditions that customers agree to. This concept was given life by the PSD2, a piece of legislation that mandated European banks to provide API access to customers' account and payment information. This directive has been a game-changer, opening up a world of possibilities for third-party providers of financial services.

Companies like GoCardless and Plaid (in the US) have seized this opportunity, building the connecting infrastructure between bank data and customers. They act as the bridge, enabling a seamless flow of information and fostering an environment of financial transparency and accessibility. The result is a simpler, lower-cost approach to financial services, albeit with less functionality and control over the user experience than an experience driven by embedded banking features.

The virtues of Embedded Finance

On the other side of the coin, we have embedded finance. This refers to the integration of financial services into non-financial platforms, providing these services at the consumer's point of need. The idea is to solve more problems for customers, thereby increasing revenue and product stickiness. It's about making finance a seamless and pleasant part of the customer journey, rather than a separate, disjointed experience.

Banking-as-a-Service (BaaS) providers, such as Swan, are the enablers of this embedded finance revolution. They offer a platform that companies can leverage to embed finance into their product suites. By piggybacking off of Swan's regulatory model and payments APIs, companies can offer their customers accounts, cards, payment orchestration, and more, without the need to navigate the complex regulatory landscape themselves.

The beauty of BaaS lies in its simplicity. Providers take care of the complicated stuff, allowing companies to focus on what they do best: delighting their customers. The power of embedded finance truly lies in combining an excellent understanding of end users with financial services that get the job done. It's about creating a seamless, integrated experience that meets customers where they are.

User experience will be decisive for the future of banking

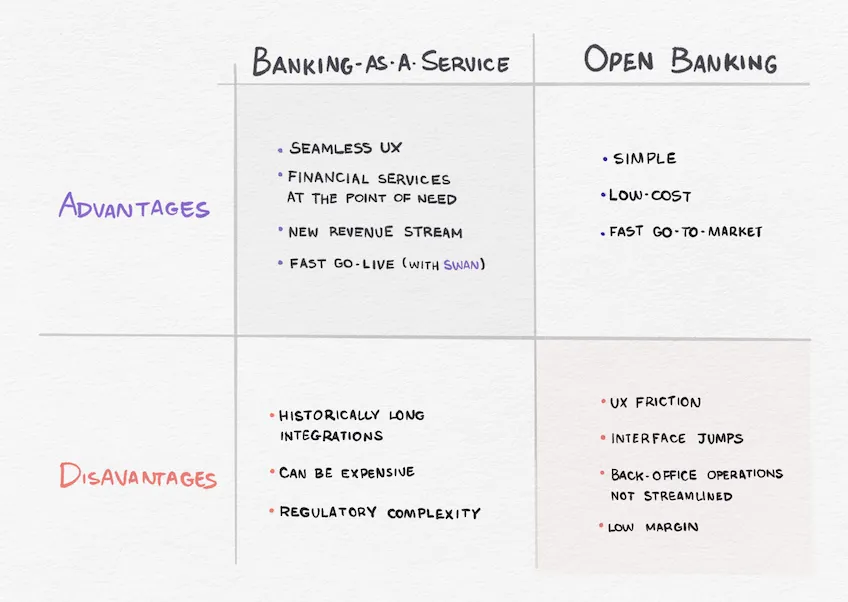

Embedded finance and open banking represent two significant shifts in the financial services landscape, each with its own set of advantages and challenges. Embedded finance, at its core, is about integrating financial services directly into a company's product suite, often through a BaaS provider like Swan. This approach offers a seamless customer experience, as it allows users to access financial services at their point of need, without having to navigate away from the product they are using. Moreover, it opens up new revenue streams for companies, as they can monetize these additional services more directly but, of course, must also pay enabling technology providers.

However, the challenge lies in the complexity of implementation. Until very recently, embedding finance has been a time-consuming process, requiring significant resources and expertise to build customized features. Clients would need to pursue a regulatory license that could take up to a year while devoting considerable engineering resources on feature development.

Open banking has always been a bit more modest in its ambition. The purpose was first and foremost to compel traditional banks and financial institutions to embrace technological developments. Banks must offer API access to customer data; third party companies emerged to provide the infrastructure linking customers to their banks in a scalable and effective way. Governments were saying to the banks: “Hey guys, please join the 21st century and hire software developers!”

Open banking products often carry with them a significant degree of friction. Users might have to negotiate a series of interface jumps as they are pushed through the product’s UI, leading to challenges with retention. Friction continues even after a successful first connection because of regulatory requirements that mandate re-authentication every 90 days. Finally, while the online delivery of financial services is innovative from a UX perspective, back office operations between financial institutions is not tangibly streamlined.

As with any business decision, there are pros and cons when it comes to choosing between Open Banking and Embedded Finance.

Open Banking offers a simpler and lower-cost approach, but with less control over the user experience. Embedded Finance, on the other hand, is best deployed when companies are looking to drive revenue generation and product stickiness.

Historically, embedding finance has been a time-consuming process, often seen as a significant barrier to entry. But Swan has disrupted this with our regulatory model, which can enable a go-live within a matter of weeks. This is a game-changer, making embedded finance a viable option for more companies and further democratizing access to financial services for consumers.

Open Banking and Embedded Finance are in many ways two sides of the same coin

In conclusion, both Open Banking and Embedded Finance represent significant strides forward in the financial services landscape. Fundamentally, embedded finance has built on the foundations laid down by PSD2-era open banking innovations to deliver a more complete, operationally streamlined, and user friendly way to deliver digital financial services. They offer different approaches to the same goal: making financial services more accessible, more integrated, and more customer-centric. As we move forward, it will be fascinating to see how these paradigms continue to evolve and shape the future of finance.

Summary

Customer stories

How Europe’s leading business platforms use Swan

.svg)

.svg)

%201.svg)

500+

Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

500+

Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

500+

Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

To use Apple Pay you need a supported card from a participating card issuer. To check if your card is compatible with Apple Pay, contact your card issuer. Apple Pay is not available in all markets. View Apple Pay countries and regions. Features are subject to change. Some features, applications, and services may not be available in all regions or all languages and may require specific hardware and software. For more information, see Feature Availability.