.svg)

The new Compte Pro: stars of French Tech are eating up embedded banking

Pennylane, Indy, Libeo, Agicap and so many other French SaaS in financial management are embedding banking services to build seamless, all-in-one solutions for individuals and businesses alike.

500,000

homeowners communities managed

80%

of property managers in Spain using it

40%

reduction of banking cost for communities

More than a decade ago, a16z declared that software would eat the world: traditional industries, from transportation to healthcare, would be disrupted by software-driven innovation. Software would become the primary driver of change and competitiveness in nearly every sector of the economy.

Fast forward ten years, and it’s clearly happened. Innovators are now looking further and there’s a new market to eat up: banking.

Embedded banking is on the rise in France

Pennylane recently became a unicorn, positioning itself alongside accountants with a real-time accounting tool designed to appeal to both businesses and accounting experts. Indy, which recently raised €40 million, focuses on freelancers, independent workers, and self-employed professionals, offering an impressive user experience.

Our neo-bank friends like Qonto have become essential for executives and a true alternative to traditional banks. In an impressive expansion strategy, they recently acquired Regate, a pre-accounting solution specifically targeting small and medium-sized enterprises and accounting firms, with powerful API tools alongside Sage and Cegid. Qonto, the leading neobank with over 400,000 clients, thus moves into the financial management realm, strengthening its offering.

Despite the trend of cost-cutting in the tech industry, neobanks and these newly converted fintech companies have managed to develop new revenue streams with their existing customers and improve their profit margins.

As embedded banking trend gains momentum, it’s not just about keeping up — it’s about seizing the opportunity to thrive in this new era for tech. Embedded banking has become a must-have for all financial tools.

Firstly, what is the value of embedded banking?

Embedded finance, overall, refers to the integration of financial services into non-financial platforms and applications. From e-commerce websites offering instant loans at checkout, to ride-sharing apps that let you pay without thinking about it, embedded finance is all about offering smooth user experiences. Embedded banking simply refers to features traditionally offered by retail banks such as accounts, cards, and payments living inside the apps and software we use every day!

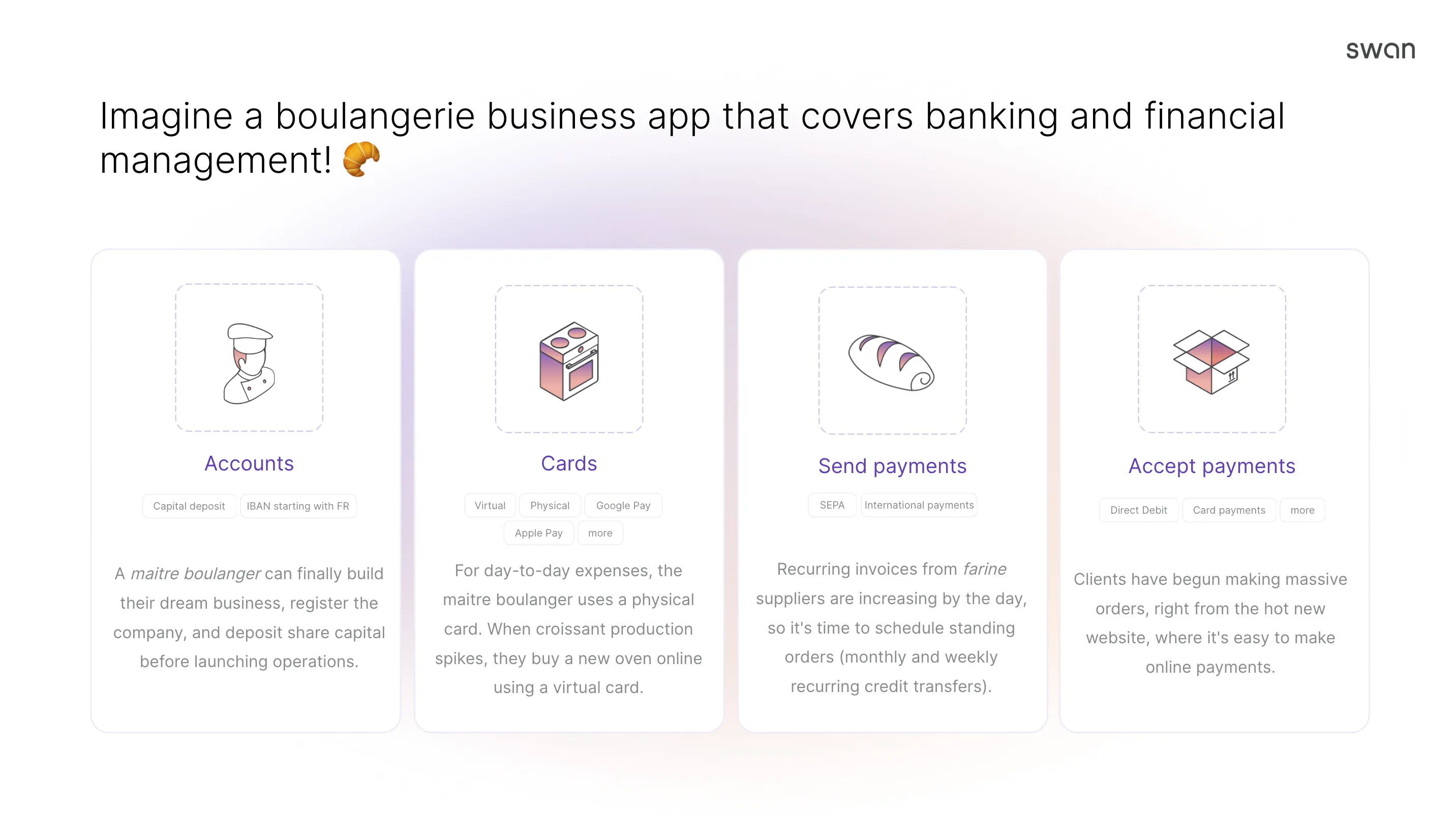

SaaS companies across all kinds of sectors are taking advantage of embedded banking. Specialized apps will provide all the same services as a traditional bank, in a much more pleasant way. Picture a management app for boulangeries 🥖. A baker would no longer have to go to a local bank branch to pay suppliers, order business cards or get a loan. It could all be done in their boulangerie management app!

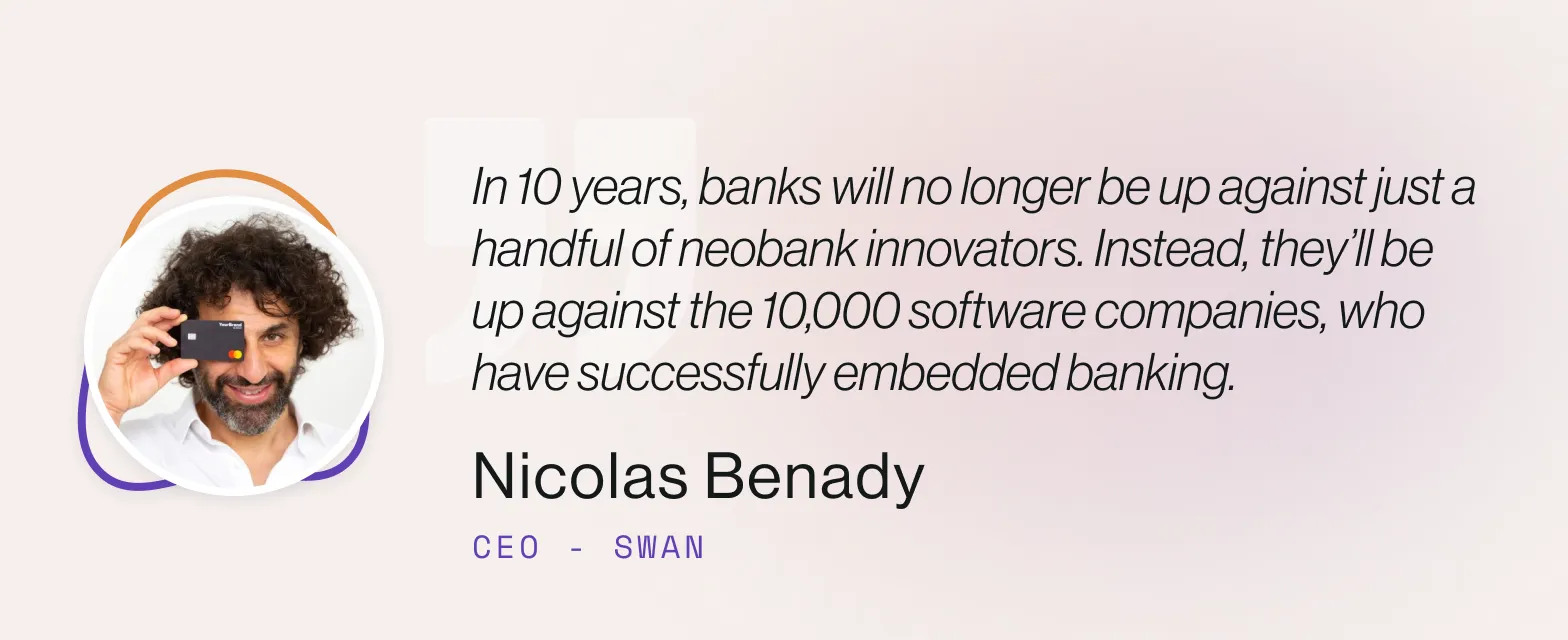

So in ten years, banks will no longer be up against just a handful of neobank innovators. Instead, they’ll be up against the 10,000 software companies, who have successfully embedded banking.

Why is embedded banking taking off in France now?

French tech is doing well. Thanks to proactive government initiatives since 2017 to establish France as a “startup nation”, the number of startups has soared to 13,000, up nearly 40% from 2016.

A supportive regulatory environment is even encouraging innovation at older, more established companies. For example, a current mandate requires all companies to accept and issue electronic invoices, to which an additional layer of invoice payments seems only natural. The reform opens market opportunities for businesses in accounting, invoicing, treasury, HR, and more, to innovate and improve.

On top of this, the barrier to entry into embedded banking is also significantly lower compared to the early days of Banking-as-a-Service (BaaS) providers. In the past, pioneering BaaS companies faced substantial hurdles, from regulatory blockers to the need for extensive infrastructure. With advancements in technology and regulation, the landscape has shifted.

Today, startups and innovators can tap into a wide array of ready-made tools through APIs offered by established players. Swan, for example, makes available web banking and onboarding interfaces that help companies launch in a matter of days. We even opened our source code, to enable a quick time-to-market with deeper level of customization - developers can quickly add, remove or tweak components from our banking interfaces.

Top banking features that financial management apps are offering customers

French financial management apps are launching their own version of a Compte Pro (read "business payment account" in English), and they have been widely adopted by freelancers and small to medium-sized companies. Here’s some common features fundamental to ensure adoption by French users:

1. Local French accounts

The first building block of embedded finance is payment accounts. And they must be localized. It’s all about the end customer experience. Whether you have a Financial Management app, HR app, Legal app — if your customers are French, when they’re opening an account they expect everything to be French. It’s a lot more than just translation. They expect French Terms and Conditions, following French laws. French payment methods. French support. They want their tax reporting to be done locally. And they want their IBANs (the account identifier) to start with “FR.”

If you’re serving end-users across multiple geographies, you’ll want to offer this localized experience for each country: Dutch, German, Spanish, etc.

Why is this so important? People trust a local IBAN. Can you imagine the eyebrows raised when a provider of the French boulengerie asks for billing info and sees a Bulgarian IBAN instead?

2. Send and accept payments

Efficient management of accounts payable and receivable is essential for any business activity. Embedding SEPA payments offers robust capabilities for automating invoicing, tracking payments, and managing cash flow, ensuring smooth and streamlined financial operations.

Swan allow our partners' clients to receive payments directly into their Swan account. Swan currently offer the widest range of receipt methods in France:

- Card: although card payments remain minor in B2B because they can be expensive, we offer this payment method as it is popular when coupled with a payment link.

- IBAN for receiving transfers and instant transfers. If a software already uses Open Banking to initiate payments for invoicing customers, for example, you can provide this IBAN to receive funds.

- SEPA Direct Debit (SDD): SDD Core or B2B. We are the only ones offering these two types of direct debit, one presenting fewer rejection risks, but at the expense of a slightly less smooth process.

- Check: It might appear trivial, but check deposits remain relevant in France and are essential for any professional account. As a matter of fact, we found on our research with Aperture that 32% more neobank customers pay with checks compared to traditional bank customers - this is an important gap that shouldn’t be overlooked.

3. Local card issuing

Empowering businesses with spend management tools is crucial for ensuring financial control, which can be achieved with both virtual and physical cards. With Swan’s payment control capabilities, financial management tools can provide branded expense cards with customizable spending limits and real-time tracking, enabling businesses to manage expenses effectively and gain actionable insights into their spending patterns.

Local card delivery is an important detail: Swan has a card issuing hub in France for the production and sending of physical cards, allowing for better delivery times for end-customers.

4. Capital Deposit

Facilitating capital deposits is a cornerstone of financial empowerment for startups and entrepreneurs. An API-available feature at Swan that is key to addressing the French market and capturing business creations, equipping them with a professional account. This feature has been proven on a large scale and is integrated by most of our partners launching a professional account.

5. Account funding

In the case of a main professional account, the IBAN is indeed the main source of account funding, whether it is proactive on the part of the account holder from a secondary account, or from customer receipts.

Setting up a B2B direct debit mandate between a secondary bank account and the Swan account. This feature offers the best possible experience as it is completely invisible to the account holder: the Swan account is automatically replenished with the desired amount without any additional action.

Recurring funding via B2B direct debit is significantly more reliable than with Open Banking. Via Open Banking, conversion rates on payment initiation are low; a recent study conducted by Powers and Fintecture among others reported an average rejection rate of 47%.

The specificities of French financial regulation

The entire difficulty of opening and maintaining professional accounts on a large scale actually relies on the execution of complex operations. At Swan, for over 3 years, we implemented and constantly improved on the following processes:

- Reporting to FICOBA: the Fichier National des Comptes Bancaires lists all bank accounts opened in France: current accounts, savings accounts, securities accounts and more. These files are managed by the Direction générale des finances publiques (DGFiP). Swan automatically declares the openings, closures, and rejection of Swan-powered accounts, updating all related banking information both in our database and public financial databases.

- Dedicated ticketing system for processing requests from French tax and judicial authorities and constant improvement of response times.

- Processing of Dematerialized SATD (Administrative Seizure at Third Party): we currently handle over thousands cases of administrative seizures completely automatically, on a monthly basis.

- Processing of bailiff cases (cas d’huissiers de justice, in French): a dedicated team is trained to handle requests for seizures in paper and physical form (represented by a bailiff).

Improper handling of these processes would expose companies embedding finance to an inability to absorb account creation volumes, operational overload related to support requests, and even possible sanctions from financial authorities.

How to get started with embedded banking

We have helped over 100 companies to structure their embedded offering. Most companies can break even between 5 and 8 months after launch, depending on the products they decide integrate. At Swan, we make it as easy as possible to build a proof of concept, validate it in the market and then build a complete banking product, layer by layer:

- Put together a banking product team and dive into documentation

- Choose your integration format and start building

- Validate product assumptions by evaluating user behavior

- Prepare your go to market strategy and communicate features’ benefits with users

- Monitor KPIs to track banking features usage and decide what to build next!

Starting with a team of 1 project manager and 3 developers could mean integration and beta launch in under 2 months. Connect with one of our fintech experts to discuss your product vision and get a step closer to making it a reality.

Summary

Customer stories

How Europe’s leading business platforms use Swan

.svg)

.svg)

%201.svg)

500+

Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

500+

Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

500+

Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

To use Apple Pay you need a supported card from a participating card issuer. To check if your card is compatible with Apple Pay, contact your card issuer. Apple Pay is not available in all markets. View Apple Pay countries and regions. Features are subject to change. Some features, applications, and services may not be available in all regions or all languages and may require specific hardware and software. For more information, see Feature Availability.