.svg)

Verification of Payee: Building safer payments from day one

Verification of Payee (VoP) brings real-time account verification to European payments, reducing fraud and misdirected transfers. Discover Swan's first-month insights.

500,000

homeowners communities managed

80%

of property managers in Spain using it

40%

reduction of banking cost for communities

Regulatory change often drives innovation, creating opportunities for fintech companies to develop solutions that elevate industry standards. A recent one was the launch of Verification of Payee (VoP), a new security feature applicable for all Payment Service Providers (PSPs) in the Eurozone, and for all SEPA Credit Transfers and SEPA Instant Credit Transfers.

Created to ensure smarter, safer payments and to prevent eventual frauds, it basically consists of a real-time account name checking service that prevents misdirected payments and potential fraud. Whether for incoming or outgoing transfers, it confirms that the name and IBAN matches with the account’s holder before a transfer.

For end users, it’s simple: it gives them the confidence that money reaches the right account, reinforcing security and error prevention, and a better experience when making payments. For businesses, it means fewer disputes, and a cleaner payment flow.

At Swan, we’ve been on top of Verification of Payee for the past months, developing a best-in-class solution to our partners, so they can count on this security feature with no effort from their side.

From design to deployment, it’s been quite a journey. One month after the official launch, we’re happy to share our learnings about this process.

What is Verification of Payee

In a nutshell, Verification of Payee is a security feature that verifies whether the account details match the intended recipient of the transaction before transfer confirmation.

Users only have to enter IBAN and payee name, and Swan’s systems will reach the recipient’s bank and return a verification result in under 5 seconds, returning one of four results: Match, No Match, Close Match, or Verification Not Possible.

Instant transfers paired with Verification of Payee deliver speed and security in one step. It gives confidence, protects against fraud, and keeps the experience fast and frictionless.

Verification of Payee in B2B payments

VoP transforms B2B payments by adding a critical layer of protection where stakes are highest.

When businesses transfer large sums to suppliers, contractors, or partners, the cost of a misdirected payment extends beyond the amount: it disrupts operations, strains relationships, and triggers complex reconciliation processes.

In that sense, the feature addresses this by confirming that company names and bank details align before funds leave the account, catching both honest errors and sophisticated fraud attempts. For finance teams managing hundreds of payees across multiple jurisdictions, this real-time verification becomes essential infrastructure: it reduces the administrative burden of payment disputes, builds confidence in automated payment flows, and creates an audit trail that demonstrates due diligence.

The result is a payment process that scales without sacrificing control, allowing businesses to move money quickly while maintaining the accuracy that B2B transactions demand.

One week results: Strong start despite technical challenges across the banking industry

- Right off the bat, Match and Close Match rates exceeded 70% in most markets, and 80% in more mature markets, proving that not only most Eurozone banks and PSPs adapted their flows in time, but also businesses were well-prepared with mostly accurate beneficiary data.

- However, there were also early rollout challenges: 10.4% of requests failed due to technical issues from banks and PSPs, often from major European institutions.

During roll-out, we measured failure rates exceeding 90% for requests to specific PSPs, typically caused by missing or incompatible security certificates, the digital credentials that enable secure authentication between payment providers. Rather than returning an error, Swan’s fallback mechanism ensures continuity: the system returns a "Not Possible" result, allowing payments to proceed uninterrupted while maintaining regulatory compliance.

In addition, Swan and Mambu, our verification and routing partner, worked closely to engage affected PSPs and expedite solutions. This hands-on approach quickly resolved the issues, increasing successful verifications for our end customers.

- Last, 15% of VoP requests made by Swan's end-users resulted in a "No-Match", highlighting the ecosystem's next challenge: reliable beneficiary data.

%20(1).webp)

The Netherlands and Germany lead, other markets were catching up fast

- Netherlands set the gold standard with near-zero technical failures, while Germany follows closely, showcasing mature VoP infrastructure.

- Other major European markets like France, Spain and Finland showed solid results, though diminished by a few major banks running into technical difficulties.

- Italian banks had a bumpy start, with nearly 19% of requests failing.

.webp)

One month in: Early technical challenges gave way to steady improvement

The transition from week one to month one tells a story of rapid ecosystem maturation. While our initial outgoing Match and Close Match rates already exceeded 70% in most markets, the real progress showed up as technical reachability improved.

- In the first week, "Not Possible" responses (including technical errors) ranged from 2.5% in the Netherlands to nearly 19% in Italy, reflecting the reality that some PSPs were still finalizing their technical implementations. One month later, these numbers dropped significantly across the board: Italy improved by nearly 9 percentage points, Finland by over 7 points, and even mature markets like the Netherlands saw meaningful gains.

This improvement wasn't accidental. As PSPs completed their deployments and resolved initial integration issues, the entire ecosystem became more reliable.

.webp)

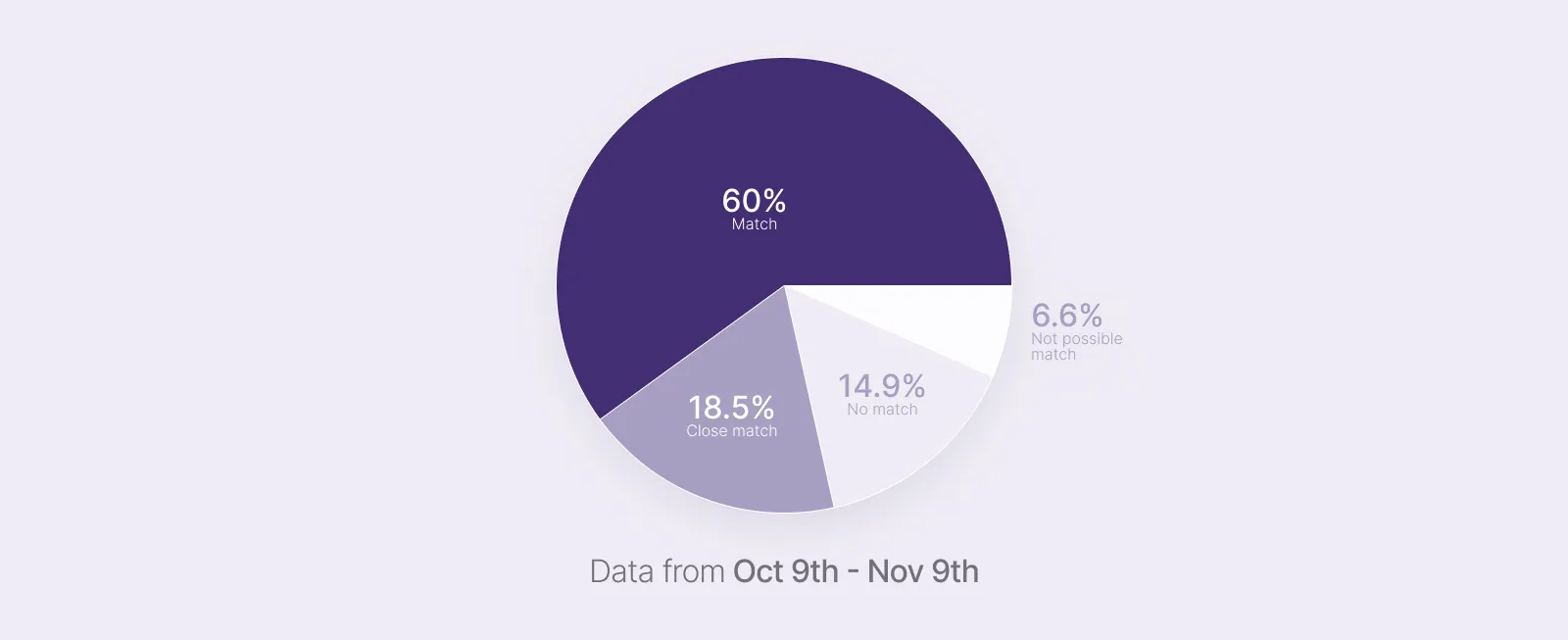

- By month's end, Swan's outgoing verification rates, measured when our end-customers initiate credit transfers, reached 60% Match and 18.5% Close Match, with technical errors dropping to just 6.6% of requests. These numbers demonstrate not just Swan's technical execution, but the broader readiness of European banks to support real-time verification at scale.

- While authentication issues have been largely resolved, the remaining 6.6% “Not Possible” rate typically stems from two distinct causes:

- Legitimate business reasons: Invalid IBANs or closed accounts, or legal identifier (e.g SIRET, VAT, etc) not supported or known by the Responding PSP.

- Technical issues: Legacy core banking systems that fail to retrieve account information within the required timeframe for real-time verification, or partial outages (which can affect any PSP’s infrastructure) leading to timeouts.

Where we stand with VoP (and why it matters)

Our VoP implementation was built in close collaboration with Mambu. Their technical partnership was instrumental in delivering the reliability and performance that powers our verification service today.

"Partnering with Swan on their VoP solution has been a pivotal moment for Mambu Payments. We pride ourselves on supporting customers to deliver best-in-class solutions, and our work with Swan is a great example of this. Our collaboration helped us to further drive innovation while raising the bar for the industry's VOP adoption, across features, stability and performance, documentation, and customer support. We look forward to continuing our work with Swan in the future."— Édouard Mandon, VP Payments at Mambu

This partnership exemplifies how strategic collaboration between banking infrastructure providers can accelerate compliance readiness while maintaining the high technical standards that modern payment systems demand.

Read more about why we chose Mambu here.

User behavior and education

Real-world usage revealed two common friction points.

- When customers transfer between their own accounts, they often enter the app or software name as the beneficiary rather than the legal name, triggering a No Match result. In these cases, we collaborate with our partners to ensure their users update the beneficiary name, and Match rates improved visibly as users corrected their entries.

- For supplier payments, customers frequently use trade names or merchant names instead of legal names, which also leads to mismatches.

Here, Swan steps in by using an enhanced matching algorithm that checks multiple name variations to improve verification success rates. This approach maximizes accuracy and minimized false results, adapting to real-world data inconsistencies to deliver matches you can trust, without adding friction.

%20(1).webp)

Beyond name matching

Today, the vast majority of incoming VoP requests validate against the account holder's name. But Swan has built for tomorrow: our solution already supports incoming verification using additional identifiers like tax numbers, company registration IDs, and SIREN numbers, all collected during company onboarding.

In practice, this means payment senders can verify recipients using legal identifiers rather than just names. While most banks haven't yet integrated legal identifier verification into their outgoing payment flows, the landscape is evolving. When the market catches up, Swan partners will be ready from day one, requiring zero additional integration effort.

In the future, we'll also enable outgoing verification using additional identifiers for more flexibility and accuracy.

Tip to win: How to raise your “Match” rates without adding friction

In a sentence: treat recipient’s data as part of your product. Set expectations with your users to register legal names instead of trade names.

If your user wants to register a new payee or add a new beneficiary IBAN, verify their beneficiary details before registering them or making payments using the verifyBeneficiary mutation.

Also, consider running end-user communication campaigns to validate and clean up beneficiary lists before payments are initiated. While there's no single shortcut to perfect Match rates, giving users the tools and guidance to maintain accurate beneficiary information pays dividends in reduced friction and higher success rates over time.

When payers make payments to your users (a Swan account), they'll also pay attention to the VoP result returned by Swan. If they receive a "No match", this may cause worry that your user isn't the intended recipient, and result in delayed payments. To ensure payment smoothness, encourage users to proactively share their own account details with payers, and prompt partners to collect additional data points during onboarding when appropriate, such as trade name, VAT number or company registration number..

Verification of Payee runs smoother with Swan

We’re very proud of what we’ve built with Verification of Payee, and we’re confident it gives you a faster path to live with compliance built in, control over the verification moment, and conversion‑friendly fallbacks while the ecosystem converges on full scheme readiness.

The net effect is less risk, fewer dead ends, and a payment experience users trust, delivered in a way that respects your product and roadmap.

If you’re refining your UX and want to keep payments smooth and secure while staying fully compliant, we’re ready to help you get there.

Summary

Customer stories

How Europe’s leading business platforms use Swan

.svg)

.svg)

%201.svg)

500+

Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

500+

Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

500+

Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

To use Apple Pay you need a supported card from a participating card issuer. To check if your card is compatible with Apple Pay, contact your card issuer. Apple Pay is not available in all markets. View Apple Pay countries and regions. Features are subject to change. Some features, applications, and services may not be available in all regions or all languages and may require specific hardware and software. For more information, see Feature Availability.