.svg)

What exactly are Banking-as-a-Service, Embedded Finance, and Embedded Banking?

Embedded finance promises the delivery of financial services in a contextualized manner via apps users are already familiar with. BaaS is one way of getting there!

500,000

homeowners communities managed

80%

of property managers in Spain using it

40%

reduction of banking cost for communities

Providing the best possible user experience to customers is essential. Software markets are competitive and in the long-run, companies that deliver delightful solutions to customer pain points will win.

We believe that embedding financial services into your product offering can often be the best way to improve user experiences while simultaneously delivering positive performance for your organization (namely, increased revenue and customer retention).

In the current market environment, where companies big and small, old and new, are competing for the attention of customers, embedded finance has emerged as one of the most powerful ways to provide defensible and profitable value to users.

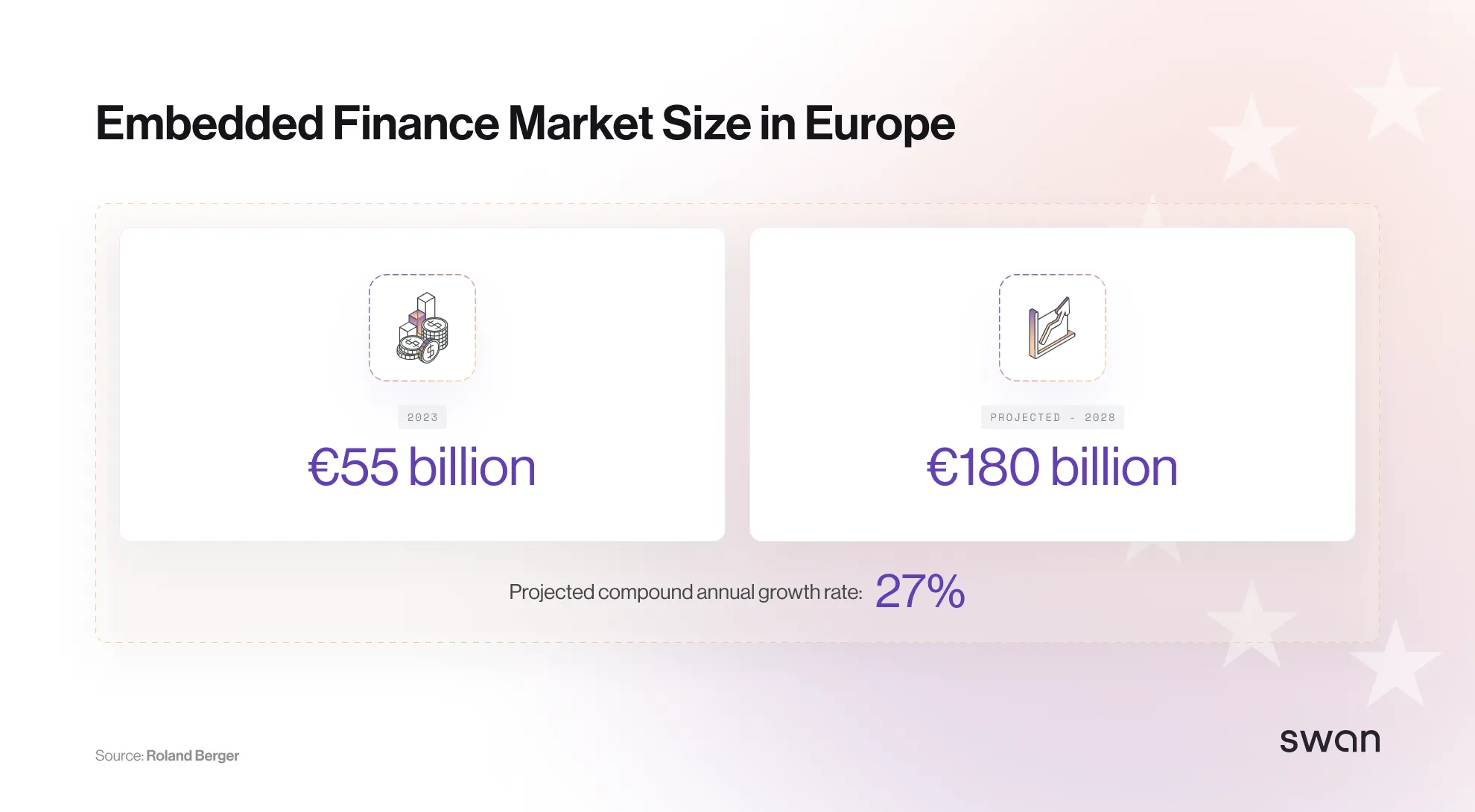

The embedded finance revolution is only at its beginning. In the future, most companies will offer embedded banking products. Today, only a relative few do. Nonetheless, the industry in Europe is already big and growing fast.

If you’re thinking about what products can supercharge your company’s growth, this guide is perfect for you. We will tackle the following key topics:

- The value embedding finance brings to businesses

- The value embedding finance brings to end users

- The difference between Embedded Finance and Banking-as-a-Service

- How regulatory decisions led to the rise of Banking-as-a-Service

- What kind of banking features you can embed into your product

- How Swan's banking infrastructure sets you up for success

The value embedding finance brings to businesses

Embedding finance delivers value for businesses in three crucial areas: more revenue, increased retention, and improved user experiences.

New revenue streams

Offering financial services alongside a core product brings a great deal of monetization potential. Our partner Pennylane built a financial management product that enabled finance teams to better organize and track invoices; customers pay a typical SaaS fee for access to the software. But you can only charge so much for that functionality.

By partnering with Swan to build Pennylane Wallet, which enables users to pay bills and invoices directly within the accounting tool, Pennylane could charge more for its software license while also earning variable revenue every time a customer makes a card payment.

Increased retention

With embedded banking features, customers just naturally will have more touch points with your product, which, of course, makes your offering stickier. Agicap, a leading financial management tool, partnered with us to enable payments directly within their core offering.

Users who once logged in to Agicap once or twice a month became, almost overnight, active multiple times a week. That’s a big change and one that can only be catalyzed by adding features that provide significant value.

Better user experience

For expense management platforms like our partner Expensya, issuing cards to users is highly motivated by a desire to level up user experience. Traditionally, expense management tools focused on the processing of invoices and receipts after users made purchases.

But issuing cards to end users, thereby removing the time-consuming process of collecting and justifying receipts, brings a UX improvement with it. For companies developing corporate expense management software, it has become table stakes to give customer’s access to payment cards.

The value embedding finance brings to end users

Most people today aren't even aware that banking products are embedded in the apps they use. Because of that, there's also not much awareness around how advantageous it is.

Interestingly enough, folks whose needs were neglected by traditional banks — self employed and small business owners — are driving interest in embedded finance!

For freelancers, solo entrepreneurs, and small businesses owners, long neglected by historical financial institutions, banking experiences embedded in software represents a revolution in UX and accessibility.

Embedded finance promises the delivery of financial services in a contextualized manner via platforms users are already familiar with. In practice, this means that a payment processor can offer financing based on the revenue data it has access to. Or that the tool a property manager uses to organize tenant information can also receive and reconcile rent payments.

Software companies are delivering a much improved customer experience with embedded banking products, which translates to a sticker offering and the opportunity for additional revenue streams.

In fact, a BCG study confirmed that 74% of SMEs would be interested in embedded payments, but only 30% of surveyed platforms were offering it.

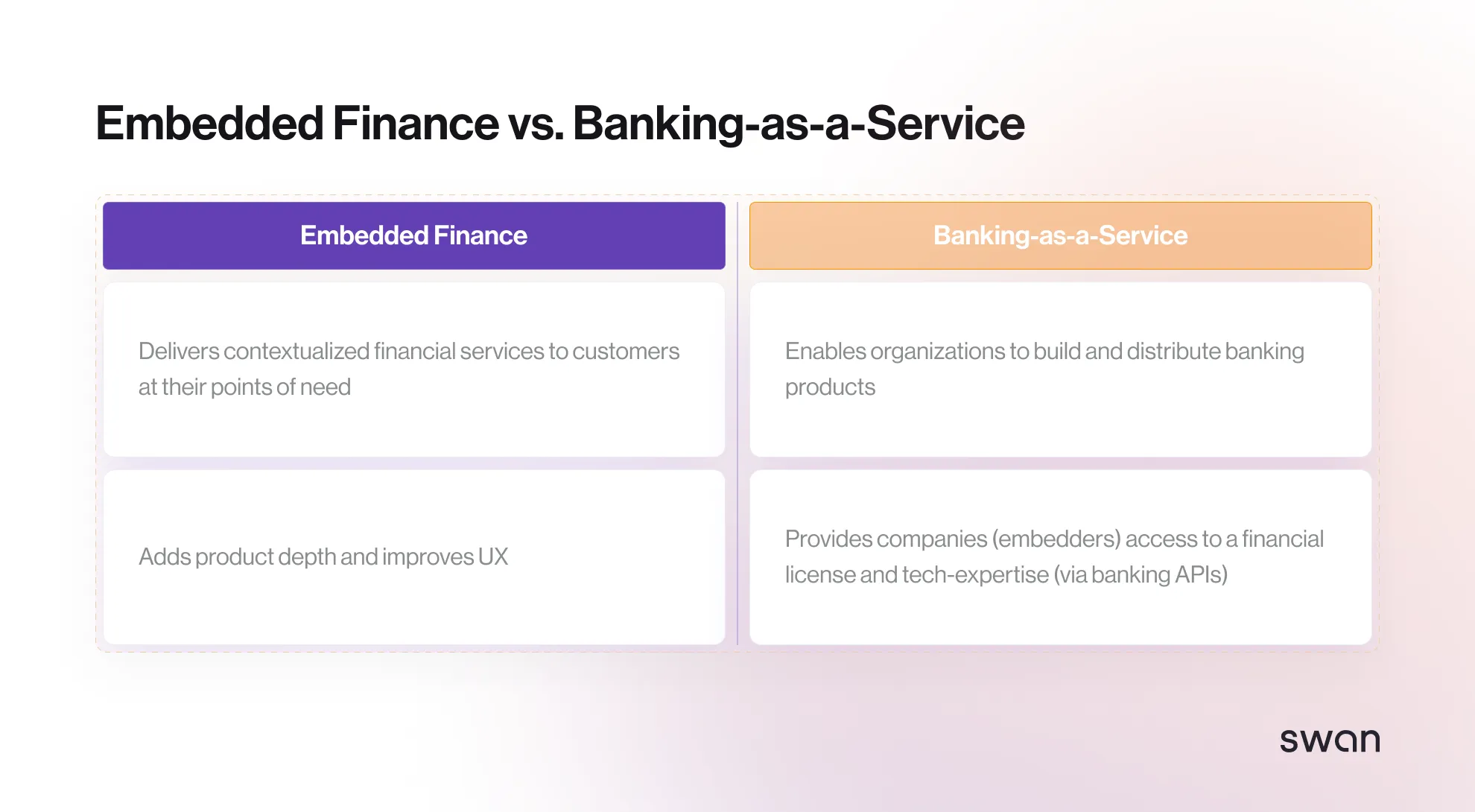

Difference between Embedded Finance and Banking-as-a-Service

Embedded finance has existed for years and does not necessarily need to involve a computer, APIs, or anything technological. Embedding finance is an activity a company undertakes to add product depth by delivering financial services to their customers at their points of need.

An example of embedded finance is receiving financing when purchasing a car at a dealership. The consumer is there to view and buy the vehicle but dealers figured out that they could also sell loans exactly at the point when the customer needs financing. This is clearly an offline example of embedded finance; it does not happen just on platforms or in apps.

Uber is a great example of a company that has embedded finance within a technology platform. Their core business was a marketplace to match people who need a ride with those who can provide one.

Cleverly, Uber embedded finance into their product by automating payment from the rider to the driver at the precise point of need, improving the payment experience for everyone involved in the transaction. Uber’s Pro Debit Card product is powered by Branch, which is an American BaaS provider. Uber itself is not allowed to issue cards; they need a regulated banking partner.

Banking-as-a-Service is a delivery method for financial products from regulated entities to non-regulated ones. A BaaS provider is a company that sells access to its banking license and tech-enabled finance expertise (think APIs) to enable other companies to embed finance.

It’s also important to note that embedded banking, a term commonly used, represents a subset of the wider embedded finance world. Embedded banking usually refers to more traditional products offered by banking organizations, such as accounts, debit cards, and payment services. Embedded finance is broader, including things like insurance, investment accounts, and FX that are not always offered by typical banks.

BaaS came to life once certain regulatory and technological developments happened to make the B2B delivery of banking capabilities possible. Let’s dive a bit deeper into this now.

How regulatory decisions led to the rise of Banking-as-a-Service

In Europe, at least, the era of BaaS started with the announcement of Payment Services Directive 2 (known as PSD2) in 2016. The primary purpose of the legislation was to force European financial institutions to modernize by allowing third party providers to access consumer banking data. Banks had to hire developers and began to properly focus on how to leverage technology.

Suddenly, a whole universe of opportunities blossomed. With engineers on their payrolls, bank leaders saw a chance to go beyond simply exposing customer data with APIs. It was time to deliver core banking capabilities (account creation, card issuing, payment orchestration) via the internet. Banking-as-a-Service as a concept was born.

Legacy financial institutions (slowly) began crafting their BaaS strategies. But a new type of entity also emerged. Entrepreneurial bankers founded new firms, obtaining banking licenses, but only with the intention of selling access to banking products to other companies, rather than to operate as a bank itself. This is how Swan came to be.

What kind of banking features you can embed into your product

As a BaaS, Swan focuses on three main banking building blocks: accounts, cards, and payments. Let’s quickly dive into what each of these things are so that we ensure we are speaking the same language 🙂

Accounts

Accounts are the fundamental unit of banking. They enable holders to store, receive, and send money.

When companies work with Swan, they can open one main account to orchestrate core payment flows often invisible to end users. For example, our partner Swile Business Travel uses a Swan account to more efficiently send money to vendors.

But accounts are more often created by our partners on behalf of their users so that they can then store money and make payments. A good case study would be Agicap, who provide accounts to their customers so that they can pay invoices directly within their app, rather than switching to another banking interface.

Bank accounts have characteristics local to the country it's issued from. Terms and conditions are dictated by a country’s government, with unique tax reporting requirements. Local accounts are important to be seen as a local player not only by clients, but vendors/providers, too.

Every account has an IBAN (International Bank Account Number). And within the European Payment Area, every IBAN works the same way, whether it’s from Portugal (PT) or from Greece (GR). However, folks often prefer to have an IBAN issued from their country as it can seem more trustworthy. At Swan, we issue IBANs from France (FR), Spain (ES), Germany (DE), and now The Netherlands (NL) as well.

Cards

Using a card is almost always the easiest way to pay. Whether online or in-store, cards just simplify transactions.

Swan’s partners issue cards to make it easier for their users to pay and manage expenses, access benefits like transportation vouchers, and just for day-to-day use as the main corporate card.

With API-driven banking, it is also super easy to generate virtual cards, which can be used for a one-time payment, for a recurring subscription, or within digital wallets like Apple or Google Pay.

For companies, issuing cards are great because they can earn revenue for every purchase a customer makes in the form of shared interchange. This, of course, would come on top of any fees that may be charged to issue the cards in the first place!

Payments

Europe boasts an excellent account-to-account payment network in the form of SEPA (Single Euro Payments Area). Embedding the capability to make payment transfers on the SEPA network is a great way to add product depth.

There are three common payment types. They are:

1. SEPA Credit Transfer

- Pay any account in the EU + some other countries

- Not instant

2. SEPA Direct Debit

- Initiate a payment to debit the account of a debtor

- Often used to pay a utility bill

- There are both B2B and B2C varieties

3. SEPA Instant

- Pay any account in the EU + some other countries instantly

- Expensive (relatively)

Many different Swan partners have added payments to their wider offering. In the case of salary advances, as an example, a company like Jump uses API orchestration to automatically make salary payouts to customers, utilizing Swan’s technology in the process.

How Swan's banking infrastructure sets you up for success

Swan is a European Banking-as-a-Service company providing access to accounts, card issuing, payment orchestration and more to companies building banking products and services.

More than 100 customers, responsible for ~€10bn in payment volume, have partnered with Swan to launch and scale their embedded finance features. We offer the fastest and easiest way to develop localized and fully compliant financial services embedded alongside existing product offerings.

Here is how:

Swan is an E-Money Institution licensed by the Banque de France. We are fully accountable for all the activities of our partners and therefore handle KYC, AML, and other important fraud prevention processes. Compliance is productized with us, so you don’t have to build it yourself.

Swan's core infrastructure was built to adapt to a fast-moving environment. We have our own ledger to process transactions and update financial records. And we are connected to the SEPA network through our own BIC & IBANs. We are a real deal financial institution.

The EU banking landscape is pretty harmonized. But there are still local particularities. We offer local accounts in Spain, Germany, and France. And make sure that onboarding processes and terms & conditions are adapted for each country’s regulatory regime. Because the local touch makes the difference.

Unlike some other companies, Swan does not force our customers into onerous long-term contracts or impose 6-figure setup fees before the project is even live. We price so that we are invested in your success: we grow when you grow.

Working with Swan, our partners are able to go live in a matter of weeks with their new financial feature, rather than the industry standard 6-9 months. We are able to deliver this because of our regulatory approach, superb customer success teams, and best-in-class APIs and documentation that make building with Swan a breeze.

Book a demo with us if you want to learn more. Or, even better, you can start building directly in our Sandbox to get a feel for Swan!

Summary

Customer stories

How Europe’s leading business platforms use Swan

.svg)

.svg)

%201.svg)

500+

Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

500+

Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

500+

Lorem ipsum dolor sit

Lorem ipsum dolor sit amet, consectetur adipiscing elit.

To use Apple Pay you need a supported card from a participating card issuer. To check if your card is compatible with Apple Pay, contact your card issuer. Apple Pay is not available in all markets. View Apple Pay countries and regions. Features are subject to change. Some features, applications, and services may not be available in all regions or all languages and may require specific hardware and software. For more information, see Feature Availability.