Send payments

Own every payment your users make

Every transfer, card spend, and international payment stays in your platform. You keep the context, the data, and the revenue.

Powering the fastest-growing companies in Europe

.svg)

%201.svg)

.svg)

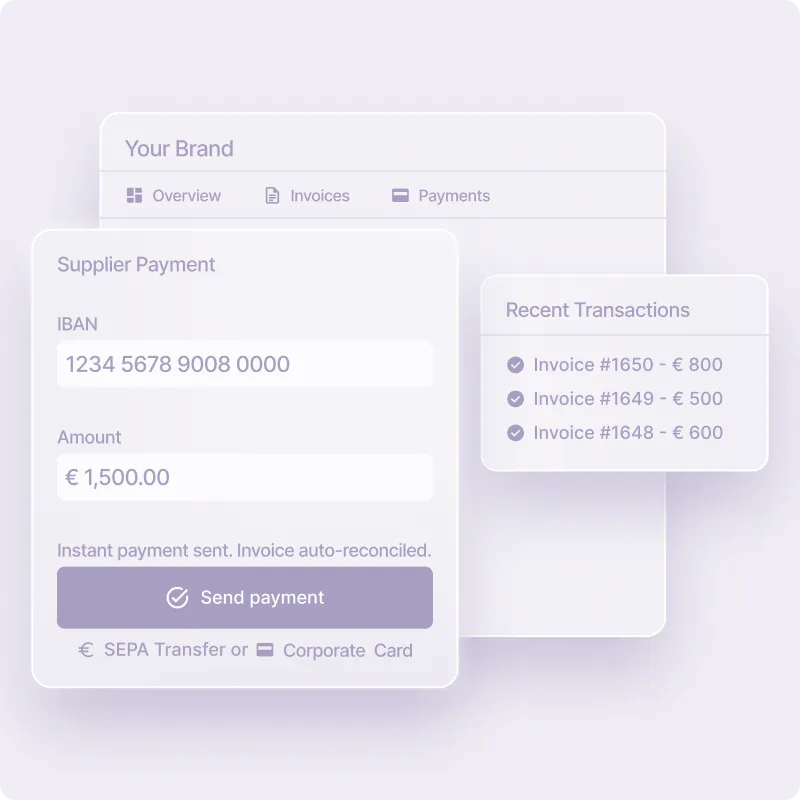

Make payments native to the work flow.

Turn every transaction into value.

Payments belong in your platform

When users leave your platform to make a transfer, you lose context, data and trust. With Swan, payments stay native: suppliers get paid, invoices are approved, and spend is tracked without switching tools.

.webp)

Transaction data that unlocks smarter automation

Match and reconcile transactions with less manual work for your users. No more export marathons, fewer “missing transaction” tickets, and a cleaner month-end close.

A new revenue stream, built into your core flow

Monetize the payments your users already make, including transfers, card spend, and international payments. Clear ROI, driven by day-to-day payment volume.

Swan in numbers

Your success is our success

From improved user experiences and retention to a more competitive product and revenue opportunities, together, we propel your business forward.

€2B

transfers processed monthly

+30k

cards issued monthly

€30M

international payment monthly

Beyond a payment button: embed the full payments experience

You own the payment experience.

Every payment your users make is a touchpoint you control, a transaction you monetize, and a reason they stay. Embedded payments turn your platform into the financial operating system your users can't work without.

- Payments are executed inside your product

- Native flow, no redirects

- One-time onboarding

- Direct access to payment rails

- Built for high payment volumes

The bank owns the payment experience

Your users step outside your product to complete a payment. Every friction point along the way is one you can't control, fix, or learn from. And as your business grows, so does your dependency on infrastructure you don't own.

- Payments are executed by the user’s bank

- Bank redirect for every payment

- Bank login and SCA

- Depends on bank APIs

- Fragile at scale

The bank owns the payment experience

Your users step outside your product to complete a payment. Every friction point along the way is one you can't control, fix, or learn from. And as your business grows, so does your dependency on infrastructure you don't own.

- Payments are executed by the user’s bank

- Bank redirect for every payment

- Bank login and SCA every payment

- Depends on bank APIs

- Fragile at scale

The bank owns the payment experience

Your users step outside your product to complete a payment. Every friction point along the way is one you can't control, fix, or learn from. And as your business grows, so does your dependency on infrastructure you don't own.

- Payments are executed by the user’s bank

- Bank redirect for every payment

- Bank login and SCA every payment

- Depends on bank APIs

- Fragile at scale

Benefits

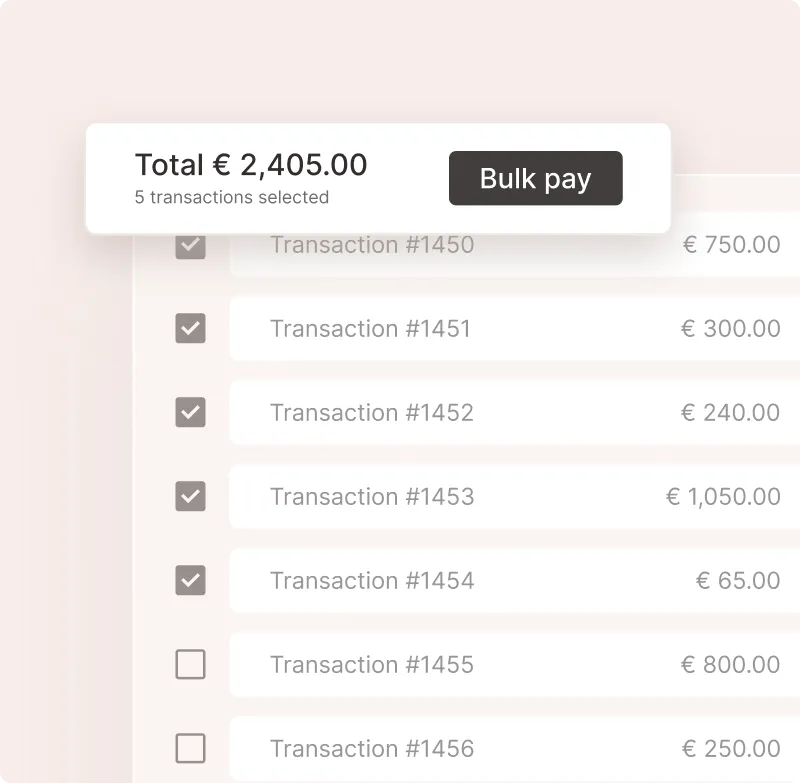

All the payout flows your users need

SEPA Transfers

.svg)

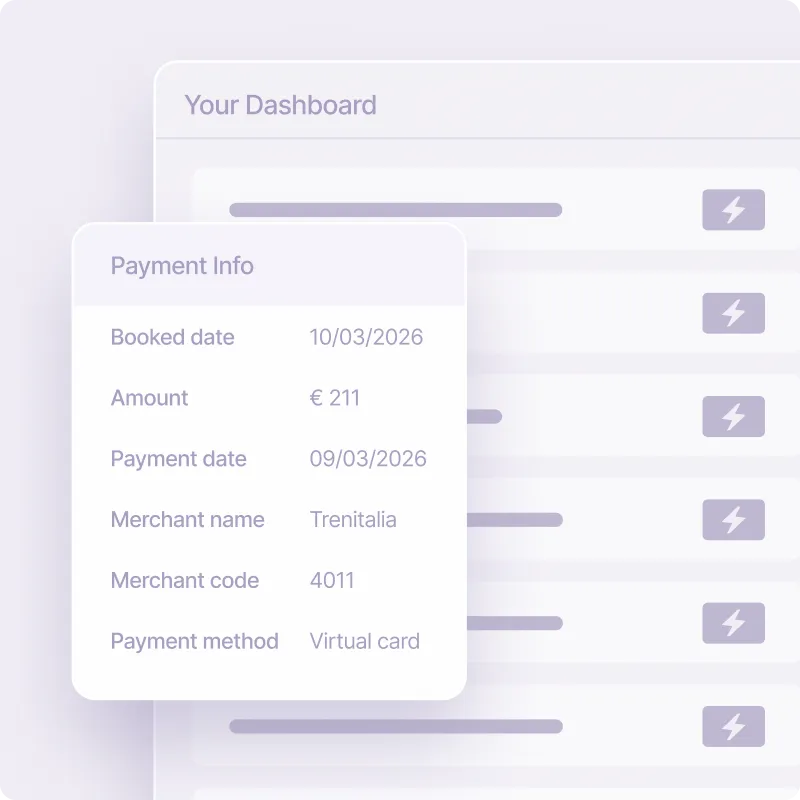

Corporate Cards

International Payments

Premium card

Cards that match spenders’ needs

.webp)

Payments work best when they go both ways

.webp)

Local Accounts

Give every user a local IBAN in their country. The account infrastructure that makes embedded payments possible.

Accept Payments

Collect incoming payments from customers via transfers, online or in-person card. Close the loop on your users' financial workflows.

FAQ

It’s ok to have questions

What’s the difference between initiating payment with Open Banking or embedding banking?

Payment initiation via Open Banking lets you trigger a transfer from a user's existing bank account. It sounds simple, but it comes with real structural limits.

- Reliability: PIS flows via third-party providers average around 47% rejection rates. For a platform handling supplier payments at scale, that's not a viable foundation

- Bulk payments: Open Banking doesn't work well for multi-payment runs, supplier batches, or recurring flows — precisely the use cases that matter most for accounts payable automation.

- Read-only by nature: Open Banking connects to your users' external accounts, but your users can't fully act from your platform. They can't receive payments, manage their cash, or reconcile automatically.

- No real-time reconciliation: Without a native IBAN in your product, transaction data still depends on a third-party bank's sync cadence. There's no automatic matching.

With natively embedded payments, the account lives inside your platform. It's always connected, updated in real time, and fully actionable — your users can pay, receive, and manage without ever leaving your product. Reconciliation is automatic via virtual IBANs.With e-invoicing becoming a legal requirement across Europe, the need for real-time data reliability and seamless payment flows will only grow. Open Banking aggregation won't be sufficient. Embedded banking is the only model that delivers on that promise.

Can payments be automated?

Yes. Standing orders, batch transfers, event-triggered SEPA transfers and event-triggered SEPA Direct Debit to fund the account and ensure it always has balance for companies spend are all supported.

How does reconciliation work?

When a payment is embedded and triggered directly from an invoice in your platform, reconciliation happens automatically: the transaction is matched to the right supplier invoice in real time the moment it completes. If your platform is connected to an e-invoicing provider, the process is even more seamless, as invoice data is already structured and available for matching.

When a transaction completes without a linked invoice, Swan triggers a webhook event so your platform can act: locate the corresponding invoice, or prompt the accountant or legal representative to confirm the match.

Either way, every payment ends up reconciled: automatically where possible, human-assisted where needed.

The result: accurate accounts payable aging at all times, immediate detection of duplicate or incorrect payments, and a complete audit trail ready for reporting and compliance.

How long does it take to integrate?

Send Payments is available via API with ready-made UI components, so you don't have to build the payment experience from scratch. Most integrations go live in weeks, not months. You can start with a single payment type: SEPA transfers, for example and then add cards or international payments progressively as your use case grows.

Is embedded banking compliant with e-invoicing regulations?

Yes, and it's actually a key advantage. As e-invoicing mandates roll out across Europe (France, Germany, Spain and beyond), platforms will be required to handle structured invoice data with real-time reliability. Open Banking aggregation won't meet that bar: it depends on third-party data sync and has no built-in reconciliation. An embedded account natively connected to your invoicing flow is the only model that can meet the legal and operational requirements of e-invoicing at scale.

Payments belong where the work already happens.

Businesses across industries are embedding financial services directly into their platforms, creating seamless, integrated experiences for their users.The future of finance is embedded, the future of your product is with Swan.